The PPF account has proved to be very effective due to good interest rates, easy rules of opening, depositing and withdrawals rules compare to Bank FD account. This is an account that any Indian citizen of any age can open and take advantage of it. In this article we are giving complete information about PPF Account Rules in 2022.

What is a PPF account?

PPF Account is a small savings scheme of Government of India. That maturity period can be 15 years. In this way, you have the freedom to make small deposits. One can deposit a minimum of Rs 500 and a maximum of Rs 1.50 lakh per year. After 15 years, your deposit is refunded with interest. In case of any urgent need there is a facility to withdraw money or take loan before maturity.

New rules of PPF account?

Any Indian citizen above 18 years of age can open a PPF account. You can open a PPF account at post office or bank branch by depositing only 100 rupees. After that, it is mandatory to deposit at least Rs.500 per year, a maximum of Rs 1.50 lakh can be deposited annualy.

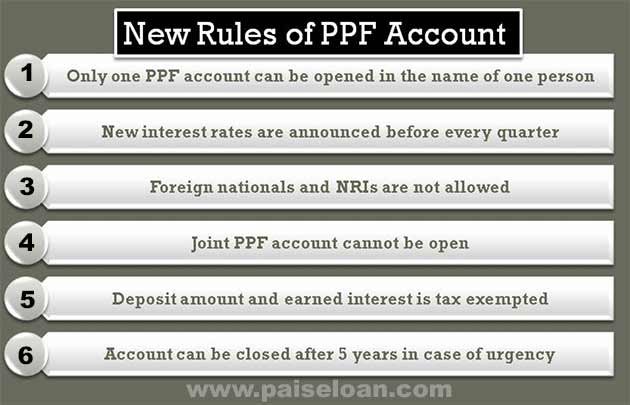

Only one PPF account can be opened in the name of one person

An individual can only open a PPF account in his name. This account is open to individual customers only, PPF account is not allowed to be opened in the name of HUF (Family Unit).

Account can also be opened in the name of the child: A PPF account can also be opened in the name of the child, but the name of the parent or legal guardian must be registered in the account. The account will be maintained by the parent until the child reaches the age of 18 years. Then it is treated as a guardian, not as a joint account.

Can also be opened for a mentally weak person:

Similarly, a PPF account can be opened on behalf of a parent for a mentally weak, deformed person. The responsibility of managing the account of such person rests with his guardian. Parents can also use the benefits of withdrawing money, taking loans, etc.

Joint PPF account cannot be open

In most government savings schemes, two or three persons are allowed to open a joint account, but not a joint account with a PPF account. However, as the guardian of your child, you can add your name to his / her account.

Foreign nationals and NRIs are not allowed

NRIs and foreign nationals are not allowed to open PPF accounts. However, if you have opened a PPF account while you are an Indian citizen, you can continue up to its validity (15 years). After maturity, you will not receive an account extension.

Note: Before 2018, once an Indian resident acquires citizenship of another country, his PPF account is automatically closed. However, the government later relaxed the restriction, allowing pre-opened PPF accounts to continue until maturity. In October 2017, the Government of India also issued a notification in this regard.

New interest rates are announced before every quarter

Currently in February 2022 the interest rate applicable on PPF account are 7.1% annually.

It is worth mentioning that just like the PPF account; the Government of India announces new interest rates on all its small savings schemes before every quarter. Some of these schemes are operated only by post offices and some are also conducted through bank branches in addition to post offices.

Schemes that can be operated from both post office and bank, their deposit, withdrawal, interest rate, tax exemption rules are the same. No bank can make different rules for these. Such as PPF Account, Sukanya Samrudhi Account, Senior Citizen Savings Account, NSC, Kisan Bikash Patra etc.

Deposit amount and earned interest is tax exempted

The PPF account is kept in Triple Tax Exemption EEE (Exemption Exemption Exemption) i.e. completely tax free schemes. In other words, its deposits, interest and maturity amount have all been kept tax free. The rules for tax exemption on these items are as below.

- Tax Exemption under 80Con PPF Deposits: Under Section 80C of the Income-tax Act, a fixed investment and expenditure of Rs. Deposits in PPF accounts also fall into this category of investments. That is, if you have not invested in any other scheme with the benefit of Section 80C, then you can avail tax exemption on the annual deposit of Rs 1.5 lakh deposited in the PPF account.

- Tax Exemption on Interest: The government does not consider interest on PPF account as taxable income. The entire interest received is tax deductible.

Tax Exemption on Withdrawal and Maturity: After 5 years of PPF account, no matter how much money you withdraw, there is tax exemption from the government. The benefit of this tax deduction is also available on the amount of maturity obtained after 15 years. But be careful! If you withdraw money by closing the PPF account 5 years ago, the withdrawn money will be considered as your taxable income.

The term of the account can be extended for another five years

Originally PPF account for 15 years. But even after 15 years, if you want, you can extend the term of your account for the next 5 years. Upon completion of those 5 years, the term of the PPF account can be extended for the next 5 years. Similarly, the term of PPF account can be extended as many times as desired by you for 5-5 years on its completion. You can also avail this account extension in two ways.

Extending the term by closing the installment in the PPF account

If you do not withdraw money from the PPF account after 15 years of maturity, your account will be automatically extended for the next 5 years. You do not even have to apply at the bank or post office.

Even during this extended period, you will continue to receive fixed interest rates on deposits in PPF accounts. However, keep in mind that with this type of automated account extension, if your PPF account is active for one year without depositing money, you will not get the benefit of depositing money later.

You will also be able to withdraw money from your account once a year. However, there will be no limit on how much money will be withdrawn. You can make as much money as you want.

Term extension through continuation of installments in PPF account

If you wish to proceed with the PPF account by depositing money after maturity, then within 1 year, you need to apply at the bank or post office where the account is located.

If you continue to deposit money without submitting the form, it will not be considered as regular and no interest will be paid on it. The benefit of tax exemption under section 80C will also not be available on it.

With the application, once the money is deposited, you will continue to accrue interest even if you continue the account without depositing money. Under section 80, tax deduction can be taken on that deposit.

Full money with interest is refunded after fifteen years

After 15 years maturity, you can withdraw full amount from PPF account. If you do not need to withdraw money at that time, you can extend the account for the next 5 years. We have already explained the rules regarding account extensions.

Account can be closed after 5 years in case of urgency

In case of any compulsory requirement, you can withdraw money from the PPF account even before the maturity of 15 years. Withdrawals from the PPF account can be made only after the completion of five financial years. That is, 5 full financial years have passed between your account opening date and withdrawal date.

For example, you opened a PPF account on January 10, 2020. Now if you want to withdraw money after January 10, 2025, you cannot withdraw. Because the years of this reckoning are calculated from the 1st of April, the date of commencement of the financial year. That is, you will complete 5 years of your PPF account on March 31, 2025. After that you can withdraw money.

Even after 5 years, few essentials can be withdrawn on following situation.

For the treatment of serious illness: PPF account holder himself, his wife, dependent. Funds can be withdrawn from the PPF account for the treatment of serious or fatal illness of the son, daughter and dependent parents. In such cases, along with the withdrawal application, you will need to submit a certificate issued by the appropriate medical authority and supporting documents to substantiate your claim.

For higher education: PPF account holders can also close the account before maturity and withdraw full funds for higher education of themselves or their dependent children. You can withdraw PPF money to study at any recognized institution located in India or abroad. Even in such a situation, in order to withdraw money and close the account, appropriate documents related to admission have to be submitted to the concerned educational institution.

Note: In case of premature withdrawal, you are allowed to withdraw up to 50% of the account balance before one financial year (at the end of the fourth year). But if the balance at the end of the fifth year is less than the balance at the end of the fourth year, only the amount which is less can be lifted.

Loan facility is also available after completing 2 years.

After two full financial years have elapsed since the opening of the PPF account, the facility of borrowing has also started from the third financial year. This facility will be available till the end of the sixth financial year. With the commencement of the seventh financial year, the facility of partial withdrawal from PPF account started and the loan facility stopped.

Can take up to 25% of previous year’s balance: Loans from PPF accounts are also available up to a limit. Up to 25 per cent of the amount deposited in your PPF account at the end of the financial year prior to the date on which you are applying for the loan, you can take it as a loan.

One percent higher interest to be paid: For loans taken from PPF account, you have to pay 1 percent higher interest rate than the applicable interest rate on PPF account. Earlier it was 2 per cent higher than the interest earned on PPF deposits. In December 2019, the government made a number of changes to the PPF scheme, including reducing interest rates on loans by 1 per cent to just 1 per cent.

Loans must be repaid within three years: Loans from PPF accounts must be repaid within 36 months from the date of receipt of loan. However, you can pay in installments as per your convenience. These installments do not have to be equal and do not have to be deposited every month. You can deposit as much as you like, whenever you want. But the entire loan has to be repaid within 36 months.

6% higher interest on the loan after three years: Even in case of loan repayment, you have to pay the full principal amount of your loan first, then only interest will be paid. It is compulsory to repay the entire interest of the loan in 1 or 2 installments. If the entire loan with interest is not repaid within 36 months, the remaining amount will attract an interest rate of 6 per cent more than the PPF interest rate, which was only 1 per cent higher in case of timely repayment.

What is the interest rate of SBI PPF in 2021-22?

PPF interest rate in State Bank of India 2020-21 is -7.1% per annum (annual). This interest rate is applicable from April 2020. This did not change until December 2021. Other key features of PPF account interest rates are as follows.

New interest rates for PPF are announced quarterly :

The Government of India announces new interest rates for all its small savings schemes before each quarter. PPF accounts also come under the Small Savings Scheme. Over the last few quarters, the government has not changed the interest rates on PPF accounts and other small savings schemes.

Prior to April 2020, the PPF account interest rate was 7.9%. Which was reduced to 7.1% for the April-June 2020 quarter. After that, interest rates remain unchanged until December 2021.

The interest on the PPF account is credited at the end of the year (annual compounding): The amount you deposit into the PPF account throughout the year is calculated on the basis of the monthly deposit. But that interest is not credited to your account every month. Rather, it occurs at the end of the financial year, i.e. at the end of March. Thus, the next year’s balance is included with the opening balance. More interest is added on it on the basis of compound interest.

Further interest on deposits calculated before 5th of every month:

Interest is calculated on the minimum balance in your account between the 5th and the last date of any month. This means that if you want to get more interest on your PPF account, you have to deposit money before the 5th of the month. If you deposit money between 1 to 5 April every year, you will get the benefit of maximum interest.

The interest rate of PPF is the same in all banks:

We have mentioned above that PPF account comes under the Small Savings Scheme of Government of India. It is enforced by all public and private banks in India, regardless of the interest rates and rules set by the government. The same interest rate and rules apply to PPF account opened at Post Office. Therefore, it is better to open a PPF account only in the bank where your savings account is already opened.

Interest earned on PPF is completely tax free:

Any interest earned on money deposited in PPF account is completely tax free. It is to be noted that the money deposited in the PPF account is also tax deductible under section 80C.

There are various types of investments and households prescribed under section 80C, which are tax deductible on deposits up to Rs 1.5 lakh per annum. In addition to PPF accounts, such investments include Sukanya Samridhi Yojana, National Savings Certificate (NSC), Senior Citizen Savings Scheme, Tax Saving FD, ELSS, Life Insurance Premium, Children’s Tuition Fee etc.

PPF Withdrawals rules in State bank of India

Usually PPF account is opened for 15 years. That is, after 15 years you can get maturity money, but in special needs you can get half the money even after 5 years. Not only that, after 1 year you can also take a loan from PPF account. The withdrawal conditions are as follows-

- After 15 years, you will be able to withdraw the full amount of PPF (100%)

- Half (50%) of PPF money can be withdrawn after 5 years

- After 1 year, one-fourth (25%) of the deposit in the PPF account can be borrowed

- You can withdraw up to 60% from the extension account with contributions

- Up to 100% withdrawals can be made from the extension account without any contribution

Now let us discuss these rules in detail one by one.

After 15 years, full of PPF can be withdrawn

The term of PPF account is 15 years. That means you have to deposit money for 15 years. Upon completion of 15 years, your full money will be refunded with interest. To withdraw money after maturity, you need to fill out and submit the account closure form. You will also need to present your passbook.

The 15-year period for maturity is calculated in terms of the full financial year. The incomplete financial year in which the account is opened in the middle of the financial year is not included in the 15 year account. After the end of that financial year, the new fiscal year that begins will be considered the first financial year.

For example, if you opened an account on October 10, 2020, the first fiscal year 2019-20 will not be considered. Because, it will be an incomplete financial year. After the end of the 2019-20 financial year, when the new fiscal year 2020-21 begins, it will be considered the first year of your account.

Account Extension Options:

You can continue your account after 15 years if you wish. For this, you need to fill out and submit an application, to extend the account for 5 years. Rules for withdrawing money from PPF account with account extension are given later in this article.

After 5 years 50% of PPF can be withdrawn

You can withdraw half the money (50%) after 5 years of opening a PPF account. The start years of this facility are calculated for 5 full financial years. For example, if you opened an account between 2021-22, your 5th year will be considered at the end of 2026-27. From FY 2027-28, you will get partial EPF withdrawal discount. Withdrawals are allowed only once in a financial year.

50% of Quantum’s application for partial withdrawal will not be calculated according to the amount available. Rather, it is based on money at the end of the financial year, which passed 3 years ago. For example, if you apply for a partial EPF withdrawal in FY 2026-27, you may receive up to 50% of the amount at the end of 2022-23 FY.

After 1 year, you can borrow up to 25% of the deposit in PPF account

You can take a loan from your account 1 year after opening a PPF account. You can get a loan up to 25% of the amount in your PPF account. At the end of the financial year two years prior to the date of application, you will receive a loan of up to 25% of the balance in your account. For example, if you apply for a loan between 2022-23, you can get a loan up to 25% of the balance in your account on March 31, 2021.

Loan facility is available from PPF account only once in a financial year. The second loan facility is available only when you repay the previous loan.

The 1 year term for the loan will be calculated according to the full financial year. For example, if you open an account in 2020-21, you will be able to avail the loan from 2012-13 financial year. The loan facility is closed after 5 years of the account. Because after 5 years the facility of partial PPF withdrawal starts. We have given the rule of partial withdrawal from PPF account in the next paragraph.

If you repay the loan within 36 months of taking the loan, you will have to pay interest at the rate of 1% per annum. If the loan is repaid after 36 months, interest will be paid at the rate of 6% per annum.

Rules for withdrawing PPF after account extension

Even after the expiration of 15 years, you can extend the PPF account for the next 5 years. After that 5 year period expires, the account can be extended again for the next 5 years. You can do this any number of times. You can make this account extension while continuing to contribute. And, you can do this without contributing. In the extended period, the rules for withdrawing money from PPF account are as follows.

You can withdraw up to 60% from the extension account with contributions

Even if you choose an account extension while continuing to deposit, you can withdraw money once a year. You can withdraw up to 60% up to the last maturity date of your account.

You can withdraw up to 100% from one account without any contribution extension

If you choose to extend your account without depositing money, you can withdraw as much as you like. Even if you want to make full money (100%), you can make full money. However, in any 1 year, there is a relaxation in withdrawing money only once.

Can the account be closed in case of emergency?

PPF account can be closed after 5 years for certain requirements. In that case, you will get a full refund after deducting 1%. This type of emergency can be any of the following-

- In case of serious illness of the account holder. In case of serious illness of his wife or children.

- For the higher education of the account holder. Or for the higher education of his children.

- In case of acquiring citizenship of another country. Or to be an NRI.

- In case of death of the account holder: In case of emergency, the account is closed in case of death of the account holder. In such a case, the full deposit will be refunded to the person registered as a nominee in your account.

FAQ on PPF Account

Ans. You can open a PPF account at a post office or bank branch. Note here that PPF accounts are only allowed to be opened at designated or approved bank branches. Some small branches may not have the facility to open PPF account. You can go to that branch and ask about this facility.

Ans. Currently, there is no facility to open a PPF account online, however, you can download and submit the PPF form online. However, once a PPF account is opened, you can deposit money online.

- Read Also.